Shares of Deepak Nitrite Ltd took a significant hit on Friday, plummeting 15% in response to a disappointing Q3FY25 earnings report. The lackluster performance raised concerns about potential downside risks to analysts’ forecasts, which had previously projected a steady net profit growth trajectory from FY25 to FY27.

Table of Contents

Struggles to Meet Net Profit Projections

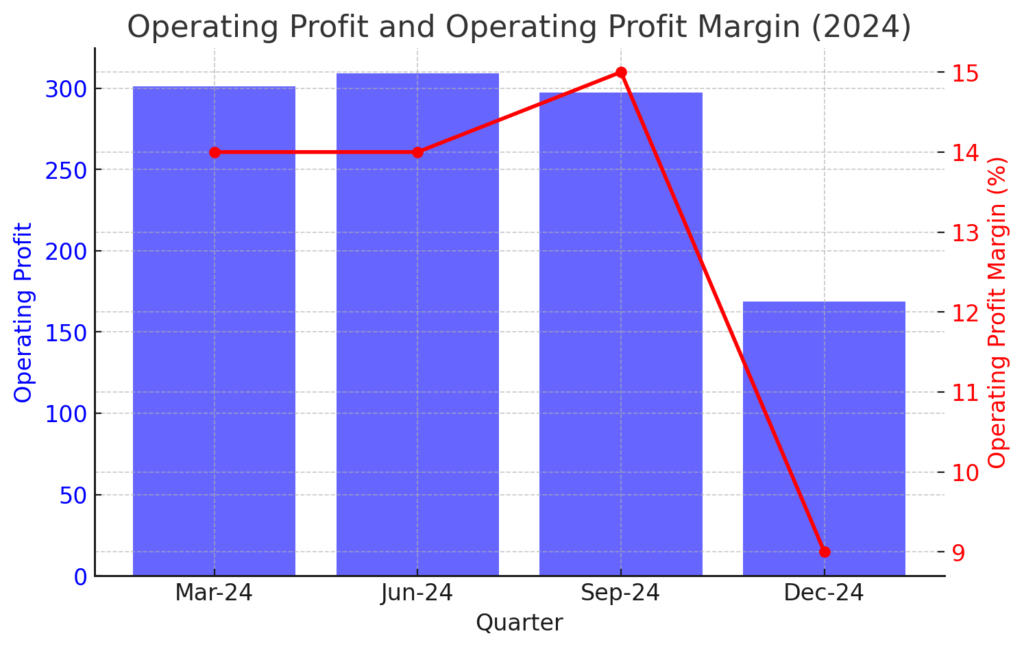

According to Bloomberg consensus estimates, Deepak Nitrite’s net profit for FY25 is projected to reach ₹814 crore. However, achieving this target appears increasingly challenging, especially considering the company’s Q3 net profit stood at an unusually low ₹98 crore. Even if the company doubles its Q4 earnings, the full-year target remains ambitious. For perspective, net profit for the first nine months of FY25 (9MFY25) was ₹495 crore, highlighting the significant gap that must be bridged.

Dual-Impact on Business Segments

Deepak Nitrite’s business operates across advance intermediates and phenolics, typically behaving counter-cyclically, meaning when one segment slows, the other usually offsets losses. However, Q3FY25 saw both segments struggle simultaneously, compounding the company’s financial woes.

- Advance intermediates segment: The Ebit margin in this division nosedived to a historic low of 3.1%, a dramatic decline from 13.9% in Q3FY24.

- Phenolics segment: Margins also compressed significantly, dropping from 13.3% in Q3FY24 to 8.9% in Q3FY25.

Key Challenges in the Advance Intermediates Business

The advance intermediates segment primarily serves the agrochemicals, dyes, and pigments industries. However, multiple external factors have impacted its growth:

- Global Destocking in Agrochemicals: The agrochemical industry has seen global destocking of finished goods, which adversely affects intermediate suppliers like Deepak Nitrite. The company believes that this impact is temporary, occurring with a quarterly lag, and expects a demand revival as inventory levels normalize.

- Dyes & Pigments Market Pressure: The intermediates used in the dyes and pigments sector underperformed due to cheap imports flooding the market at unviable prices. While the government has initiated an anti-dumping investigation, the timeline and likelihood of protective duties being implemented remain uncertain.

Phenolics Segment Faces Margin Squeeze

Margins in the phenolics segment suffered due to rising input costs. During the earnings call, the management highlighted that the current pricing spread in phenolics could pose survival challenges for non-integrated producers. However, this scenario hints at a potential recovery in phenolic spreads, offering some optimism for future quarters.

Can Profit Margins Rebound?

Despite the Q3 struggles, the company’s management remains optimistic, believing that the 8.9% operating margin could mark the bottom. They expect profitability to normalize from Q4 onward as demand stabilizes and cost-optimization measures take effect.

However, the company refrained from providing a specific margin target for normalization.

Are Valuations Justified Given Earnings Risks?

One of the key concerns among investors is whether current valuations are sustainable given the uncertainty around earnings growth.

- The stock currently trades at a 20x price-to-earnings (P/E) ratio.

- It also commands a valuation of 13x EV/EBITDA based on FY27 estimates (as per Bloomberg consensus).

Given Deepak Nitrite’s semi-commodity business model, these valuations appear expensive. Moreover, as analysts revise their earnings estimates downward following the weak Q3 results, these multiples could seem even less attractive.

What Lies Ahead for Deepak Nitrite?

Deepak Nitrite’s future hinges on multiple factors:

- Agrochemical sector recovery: A rebound in demand could revive advance intermediates.

- Government action on anti-dumping: If duties are imposed, dye and pigment intermediates could see pricing relief.

- Phenolics margin improvement: Rising input costs need to be offset with better pricing spreads.

- Operational efficiency: Cost-cutting and process optimization will be crucial for EBITDA margin recovery.

While Deepak Nitrite has faced a challenging Q3FY25, the company remains cautiously optimistic about the coming quarters. Investors, however, must weigh the potential risks against the current valuations, especially if earnings growth slows down. Until key challenges are resolved, market sentiment may remain volatile around the stock.